More on the Repo Market

More on the Repo Market

Because Government Management of Currencies Sucks

Every week in the cryptoeconomy is filled with news. Yet, the biggest story that no one is talking about is still the repo market. It affects the US economy, the dollar, and cryptocurrencies like Bitcoin. Did you read Part 1? We went into the structure of the repo market and why it’s important last week. Go ahead and check that out first. I’ll still be here with Part 2 when you’re done.

In other news, I found one interesting piece on the state of digital lending from crypto lender and OTC trader Genesis Capital

The report is a good primer on what’s going on with crypto-based lending 2.0 now that the first generation led by BTCJam (defunct), Loanbase (defunct), and Bitbond (active and growing) is done. My first interactions with Bitcoin back in 2014 were about Bitcoin lending 1.0 so I’ve always been interested in Bitcoin as an asset to borrow against. The report is free and it’s a good read about how the need for liquidity without selling BTC is in high demand and growing.

And now back to the Repo Market.

New in the Repo Market This Week

In last week’s article, we discussed how the daily intervention in the market from the Fed is now $45 billion with potential temporary increases allowed up to $120 billion. What started as a spike in the repo rate now includes daily pumps of liquidity into the system by the Fed.

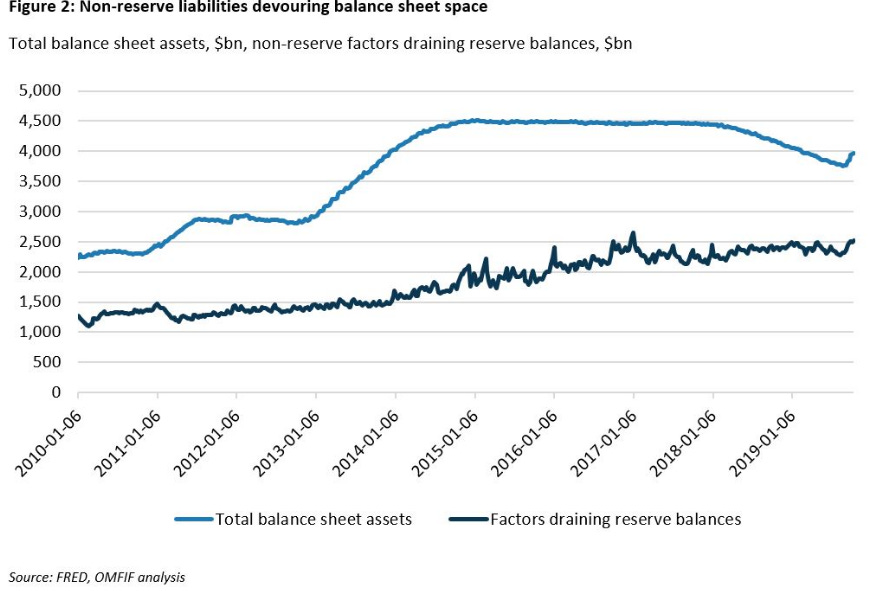

According to Pierre Ortlieb, an economist at OMFIF, the days of ‘great moderation’ in the 1990s and early 2000s were a time when the Fed kept its balance sheet in balance by maintaining the amount of USD in circulation (a liability) in line with the number of assets the Fed had on the books.

Now that’s no longer true and it’s only getting worse.

Since the Great Recession, the Fed has stepped in with lots of overnight lending, Repos, and reverse Repos to fill up the liquidity on the liability side of the Fed balance sheet for all the assets (mostly T-Bills) that the Fed buys.

Balance sheet assets during the Recession were around $900 billion and today it’s 5X that amount at almost $4.5 trillion. Just 11 years later. So it’s not a question of whether the Fed should be printing more money to get the currency circulation figure higher. They shouldn’t. If anything, both the assets and liabilities need to be reduced to more manageable levels. But that won’t be happening.

Have a friend you think might like this article? Share it with them

Almost half or ~$2.25 trillion is the amount of currency in circulation and the other half is now the Fed’s role as liquidity provider and overnight lender. These ‘non-reserve’ liabilities are growing and reserve assets, which are vital for the overall health of the US economy and markets, are shrinking. Currency circulation is different than M1 money supply. M1 is around $4 trillion.

Jeffrey Snider of Alhambra Partners sees a similarly difficult road ahead for the Fed and the USD. Here’s his short thread on Twitter describing it (FOMC is Federal Reserve Open Market Committee, the ones who decide on Fed interest rates through market purchases and sales of securities).

This Alhambra article is a good read with a little bit of an inside baseball feel to how the Fed acts the way it does. The most telling chart here is how regardless of how you look at the US economy, it still has not recovered to where we were beforehand.

The baseline growth figure of around 3% (the dotted line) shows that even with QE (Quantitative Easing) to print more USD and put it out into the market the growth numbers STILL fall short. This chart also shows how reserve balances are dropping as mentioned earlier.

Alhambra says there is zero upside risk now and lots of downside risk with limited options for the Fed when the next recession hits. Could US interest rates go negative like they have for most of Western Europe? Maybe.

Do you like real, actionable information for your cryptoeconomy investment decisions like this? For less than $2 each week, you can get this right into your mailbox.

Patrick Carvalho of the New Zealand Initiative asks one of the important questions. ‘Some market analysts are already questioning how long the Fed can sustain its money market interventions by short-term bond purchases only before moving to a wider range of Treasury maturities’. We keep hearing about a record expansion yet the Fed can’t take its foot off the gas to providing cheaper credit overnight (Repo) even with how great things are? How great is it really if the Fed must continue to prime the pump?

Carvalho thinks longer-term bond purchases are coming too. These operational techniques by the Fed to keep markets cheap and liquid are usually some of the tools used during a recession and we aren’t even in one yet. These leave fewer options to help manage the economy through the next recession when it comes.

Fed IOER is Too High

The Fed has a rate it pays banks that keep extra reserves on deposit there. These amounts are more than what’s required based on the Liquidity Coverage Rule. This Interest on Excess Reserves (IOER) is currently 1.8%. It’s a great deal for banks and banks don’t have to subject their funds to the Repo market or any risk if they can earn 1.8% just leaving their cash at the Fed. So that’s what they do.

This is another part of the Repo and market liquidity issue. Business Insider does a good job describing this activity.

While the Fed has not changed anything, if this need to provide liquidity for the Repo market continues into 2020, there’s a good chance the Fed will reduce the IOER to induce banks to lend to other banks and dealers in the Repo market.

Money printing will continue, growth will slow, and inflation will become an issue. It may not be today but it will happen.

Bitcoin’s money printing

Thanks to the algorithms Bitcoin uses, we already know exactly how many Bitcoins will be produced and what the inflation will look like. It’s the basis of quant analyst Plan B’s Stock to Flow analysis that I like and mention here often.

Bitcoin doesn’t have a government issuer. Bitcoin doesn’t need government intervention. Is that a guarantee Bitcoin will be successful? No, of course not. But Bitcoin needs to be part of your plan if you believe that governments are not capable of managing their currencies responsibly. And I believe that.

What do you think?

I also think some of Bitcoin’s value and growth will come not only from Bitcoin becoming more valuable. Also, like gold, the USD will become less valuable thanks to inflation and money printing. Bitcoin could have the same value 5 years from now that it has today. Yet instead of being $9,000 it could be $15,000 or more at least in part because it will take more of the future cheap dollars to buy a $9,000 Bitcoin in today’s dollars.

Bitcoin recently minted and released it’s 18 millionth coin out of a possible 21 million. Until May 2020, the current block reward is 12.5 BTC every 10 minutes or 1800 BTC per day. Annually that’s 648,000 BTC giving us an inflation rate of (648,000/18 million) of 3.6%. This is pretty low and it’s getting lower.

May is a little more than 6 months from now but the block reward will cut in half then to 6.25 BTC every 10 minutes or 324,000 BTC per year. Adding an additional 6 months of Bitcoin produced at the current block reward (12.5) would mean another 324,000 BTC or a total of 18,324,000. The inflation rate then will be (324,000/18,324,000) 1.76%. 1.76% is below the USD or any other government-issued currency’s printing rate for every currency on Earth. The scarcity and stock to flow models support an increase in Bitcoin’s value relative to all gov’t-issued currencies but we will need to see how that plays out over time. If that happens AND Bitcoin’s intrinsic value grows too, then you will see a high 5 or 6 figure Bitcoin price.

Do you believe the USD or EUR or CNY is being managed responsibly by those governments? What alternatives do you see besides Bitcoin and other cryptocurrencies if the answer is No?