SEC Shares Bitwise ETF Info with the Public

SEC Shares Bitwise ETF Info with the Public

Bitwise Journey to an ETF Continues

The conversation between the SEC and the crypto-economy continues. The SEC released a presentation from Bitwise that addressed some of the SEC questions and concerns from the Bitwise ETF submission request in March. Here’s a copy of the presentation.

Two of our previous articles were about Bitwise and their quest for an ETF. The first piece was when we looked at the Real 10 exchanges of Bitwise’s research. The second piece examined our and other analysis of it to ask Are We Biased?

Before we look at the new information, let’s see where we’ve been so far with a timeline.

The Timeline

While Bitwise starting filing paperwork in January. Things really started for them in March.

March 2019: Bitwise applies for a Bitcoin ETF. You can find the 226 slide presentation here in pdf format. They called it the Bitwise Bitcoin ETF Trust.

Note the March 22nd date on this. This research uncovered the Real 10 exchanges to show the SEC that the market is much closer to equilibrium than outsiders think. Equilibrium is good because that means real price discovery for Bitcoin, something we take for granted in the stock market.

May 24, 2019: Bitwise sends a comment letter to the SEC addressing initial questions from the March presentation.

June 2019: The SEC rejects the proposal from the Winklevoss twins (of Facebook fame) for their Bitcoin ETF. (A separate project)

July 2019: Bitwise announces a filing with the SEC for a cryptocurrency ETF called the Bitwise Hold 10 Cryptocurrency Index Fund. The purpose of this ETF is to be a market-weighted index of the 10 largest cryptocurrencies.

September 2019-this week: The SEC publishes a 31 slide presentation from Bitwise addressing questions and concerns. Here is that presentation.

Updates to Bitwise Presentation

The interesting thing is Bitwise didn’t release this update, the SEC did. The story broke on Forbes Crypto with Bitwise addressing 3 main areas:

The Bitcoin spot (cash) market is much more efficient now. The graph above shows the deviation in price on the Real 10 exchanges is now less than 0.10%

Bitcoin custody has become institutional. Custody is important for professional investors. Those that care about Bitcoin as an asset class but not for its privacy or independent qualities don’t care about controlling their private keys. They want to make money. And the easiest way for them is with custody. From 2017 until now, regulated custody providers increased from 3 to 9 (plus Fidelity pursuing but not approved yet).

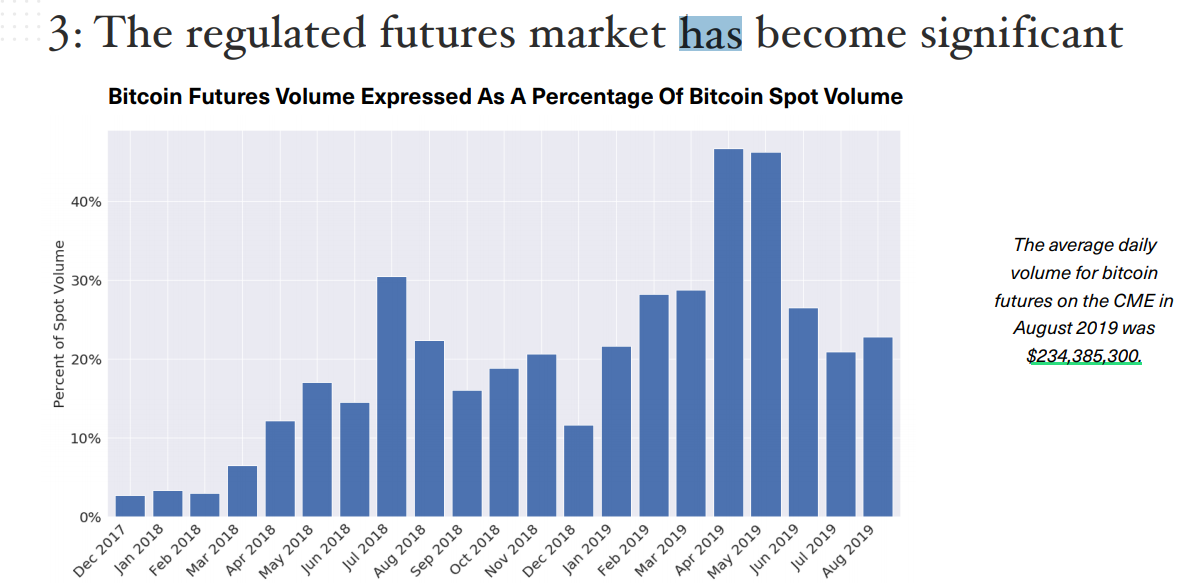

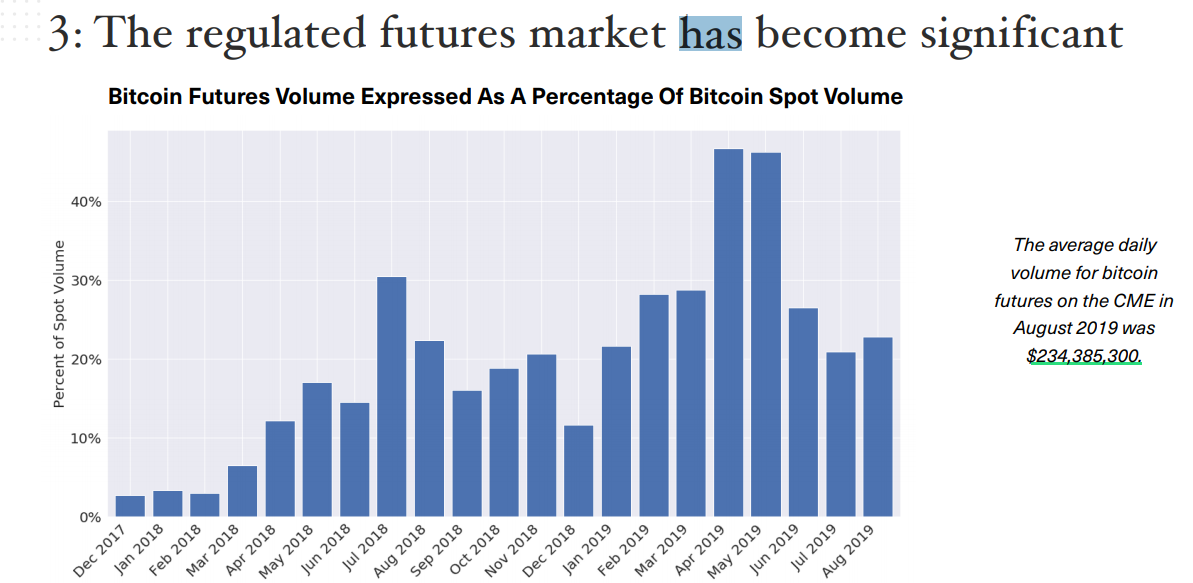

The regulated Futures market does a significant volume.

Since March 2019, the CBOE gave up on its futures contract. Now only the CME offers a licensed futures contract in Bitcoin. Yet, volumes are still increasing and volume compared to the spot market is consistent over 20% every month.

Do you like diving deeper into cryptocurrency investment opportunities like this? For less than 2 lattes you can have a month’s worth of this analysis.

The Commentary and Analysis

The Forbes Crypto story says that the SEC release of these documents ‘should not be taken as an endorsement by the regulator.’ SEC Chairman Jay Clayton said he does not see a Bitcoin ETF on a major exchange ‘anytime soon’.

One of my favorite crypto legal minds, Jake Chervinsky, checks in with a thread on Twitter.

Jake says that Van Eck, who recently withdrew their ETF proposal, was no better equipped to deal with one of the SEC’s biggest issues than Bitwise is. That issue is a lack of surveillance sharing agreements with regulated markets of significant size.

The big part of the problem for the SEC is they believe there are no markets of significant size in Bitcoin, yet.

Van Eck director Gabor Gurbacs on why ETFs are important even though they withdrew their proposal for one.

Our CNON Take: We believe that an ETF is important. An ETF equals more institutional money and access to 50% of the US investment market run by financial advisors who want a piece of Bitcoin for their clients.

We think the argument of price discovery Bitwise makes is incomplete. Why? Well, pricing is better than it was……but. The but is that of the Real 10 exchanges listed, they are US-centric. Here are the Real 10 and their primary market locations:

US- Gemini, itBit, Coinbase, Kraken, Bittrex, Poloniex (part of Circle)

Europe- Bitstamp

Japan- Bitflyer

Hong Kong/China or Singapore- Bitfinex, Binance

While all these exchanges have global presence, there is no OKCoin, Korbit, Bithumb, Huobi, Liquid and a general lack of interest in Asian exchanges.

Lastly, we think the Bitwise analysis ignores the OTC market completely. This is where the whales trade and do more volume than the exchanges do. Some of the Real 10 have OTC desks but they don’t report those numbers alongside exchange volume. This Forbes piece from June describes how OTC volume dwarfs exchange volume and BitMex alone doubles all exchange volume from the Real 10. We agree. It’s the huge volume elephant in the room. This CCN piece from July describes a study by the TABB Group that shows OTC volume at an average of 2-3x exchange volume.

It’s a number too big to ignore, especially for someone like the SEC. So while we hope the ETF will get approved, we don’t believe it will happen. At least not in 2019.

We believe it will eventually happen and be good for investors and for Bitcoin when it does.