To Halve or Halve Not?

To Halve or Halve Not?

A different theory on reduced block rewards in cryptocurrency

Strix Leviathan creates AI-based algorithms for traders in cryptocurrencies.

Like many in the crypto-economy now, they are trying to both analyze and extrapolate data to help people make better trading decisions. They recently published an article with some analysis that goes against the grain of most in the crypto-economy. Two of their researchers did an analysis of the cut in block rewards. Are they really meaningful or not?

Strix Theory: Block Reward decreases when a halving takes place have no effect on price.

While I’m not sure I believe this is true, this article made for a fascinating read so we are going to dive deeper into it this week.

The Conventional Wisdom on Halving

Many in the crypto-economy, including me, believe that supply and demand dynamics are at work with a halving. An in-demand coin like Bitcoin will see both demand increase and price increase as a result of a halving that cuts the supply.

Litecoin, an also in-demand coin, and the #5 market value-based coin had a price increase before both halvings to see returns drop dramatically after the first halving and returns are dropping since the early August halving this time as well.

Understanding what people generally believe to be true, let’s look at the theory in more detail.

Disclaimer: I hold the 2 largest cryptocurrencies in this analysis, BTC & LTC, and none of the others mentioned.

The Theory & The Assets Used

The Strix Theory Analyzed

The Strix theory is that the halving period itself has limited impact on price. Strix examined price and returns for the periods of 1, 3, and 6 months both before and after a halving event takes place. Their examination of Sharpe and Sortino ratios show that the returns up to and following a halving event are ‘no better than the rest of the market’.

Their daily returns chart shows that a halving period and a non-halving period are statistically the same up to 99% confidence level. Here is that chart from the article:

With a 99% confidence level and both returns showing a normal distribution (bell curve), the only real difference in the chart is that the non-halving period just has more days. No abnormal price action comes from the halving event itself.

The theory continues that through the Sharpe and Sortino ratios the returns support limited impact on price. The differing returns post-halving for Bitcoin and Litecoin support the theory. The researchers describe it this way: ‘The divergence and seemingly random results before and following a halving suggests that the underlying factors driving price is not a shift in supply and demand dynamics’.

Due to the earlier mentioned returns distribution data, the researchers believe that market sentiment alone is the reason why some perform very well after a halving (like BTC) and some less well (like LTC).

The Crypto Assets Analyzed

Strix looked at a list of 24 crypto assets and here they are:

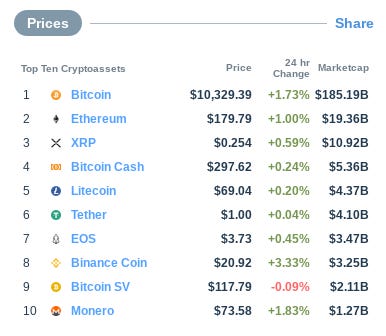

So the first thing you may have noticed is that of the top 10 cryptocurrencies by market value, only Bitcoin and Litecoin are included. I don’t know many of the names on this list and had to look them up. For instance, UNO is Unobtanium, the #251 ranked crypto by market value and whose main selling point is its scarcity. Or COLX which is ColossusXT, the #548 ranked crypto and whose goal is decentralized distributed computing like ETH or EOS but more decentralized.

Like what you’re reading so far? Get this kind of actionable information for your crypto portfolio for only $7/mo.

What Experts Are Saying

This analysis is opposed to the conventional wisdom mentioned above, meaning there’s a good chance for lots of backlash. But first, let’s start with Plan B, one of my favorite quant analysts and who has been featured twice here including last week’s 5% BTC portfolio and in BTC valuation by stock to flow models. Here’s what he had to say:

Like all of us trying to sort the signal from the noise or the news from the nonsense, PlanB believes that altcoins don’t follow the theory on block halving but that Bitcoin does.

This analysis is an attempt to quantify and tech-ify the old fashioned ‘buy the rumor, sell the news’ theory in stocks.

Here is a Bitcoin fund manager saying what lots of us are thinking when we saw the list of assets analyzed:

And then my own thoughts start with a couple of questions:

Why are only 2 of the top 10 cryptocurrencies included?

Is what we can learn from DeepOnion coin (ONION) relevant to Bitcoin?

Would a forked coin like Ethereum Classic, Bitcoin Cash, or even Litecoin perform differently than an ‘original’? And if so, why?

Are the 22 smaller cap cryptocurrencies in the study dampening the analysis we can take away for coins like Bitcoin, Litecoin, Monero, or XRP?

Is this just a case of garbage in, garbage out due to all these low-value cryptocurrencies? (Hint: I think so)

What do you think?